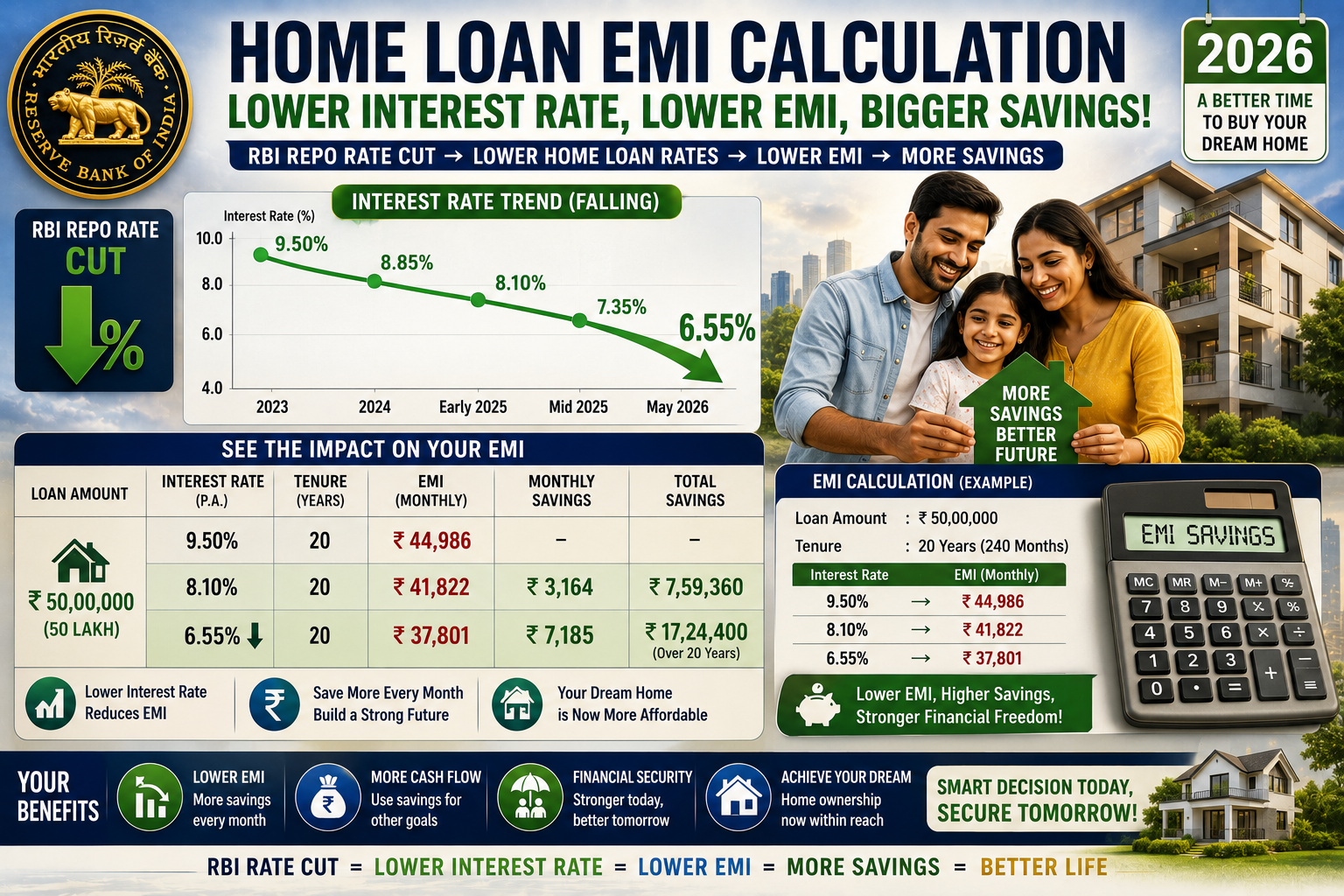

Every month, crores of Indian families sit down and calculate whether they can afford their home loan EMI. They check their salary. They check their bank balance. But very few of them check the one number that controls their EMI more than any other — the RBI repo rate. In 2025, the Reserve Bank of India cut this single number four times — reducing it from 6.50% to 5.25%. That one decision saved a family with a ₹50 lakh home loan approximately ₹3,500 every single month. If your EMI has not changed since 2024, you may be overpaying right now. This guide explains exactly what the repo rate is, how it controls your EMI, and what you should do today to make sure you are getting the full benefit of India’s most aggressive rate-cutting cycle since 2019.

🏦 What Is the Repo Rate — Explained Simply

The repo rate is the interest rate at which the Reserve Bank of India lends money to commercial banks. Think of it as the wholesale price of money. When you borrow money from a bank, the bank first borrows that money from the RBI — at the repo rate. The bank then adds its own margin and lends to you at a higher rate.

If the repo rate is 5.25% and your bank’s margin is 3%, your home loan rate is approximately 8.25%. If the RBI cuts the repo rate to 5%, your bank can pass that benefit to you — bringing your home loan rate down to approximately 8%.

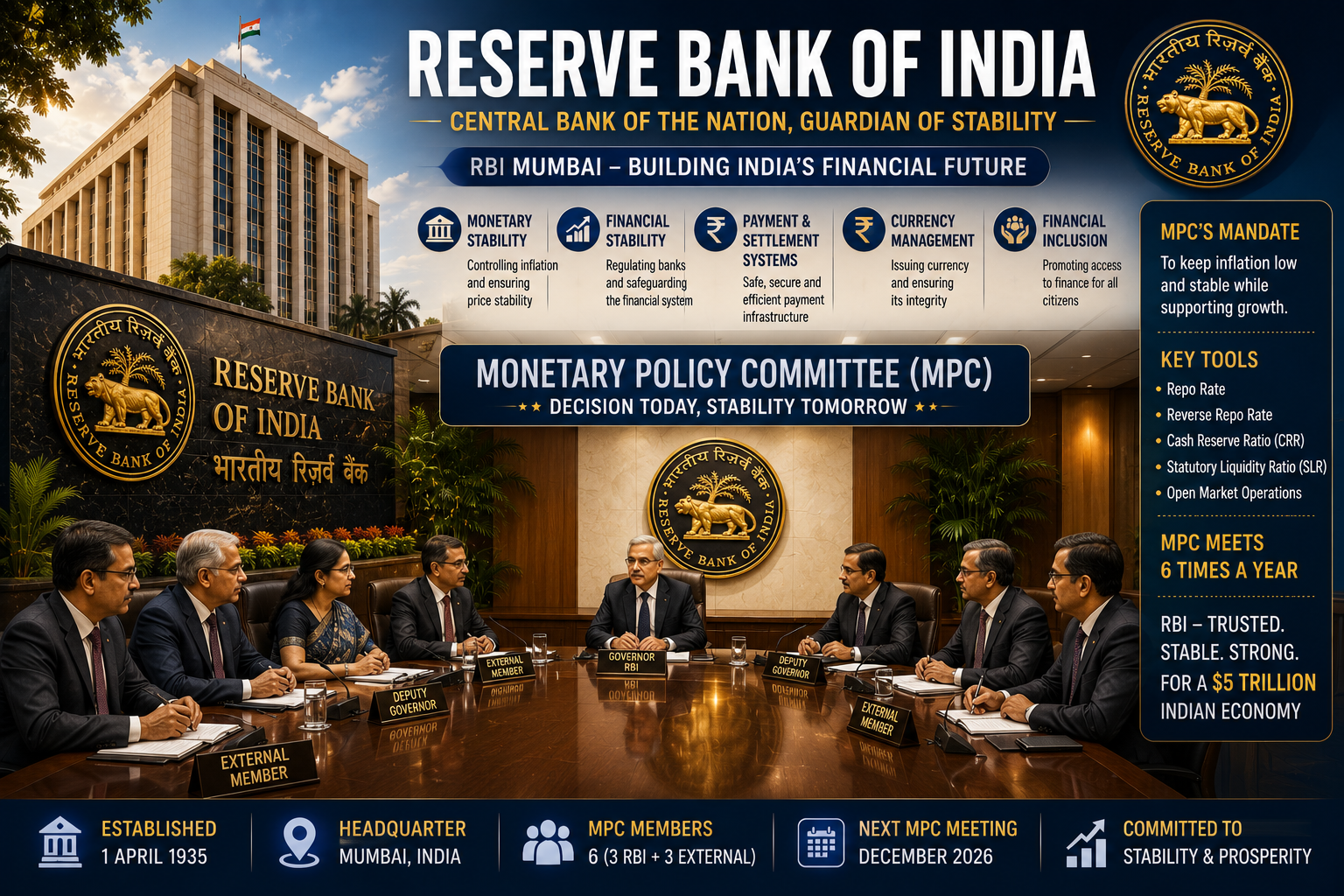

The repo rate is decided by the Monetary Policy Committee (MPC) — a six-member committee comprising three RBI officials and three external members appointed by the Government of India. The MPC meets every two months — six times a year — to review economic data and decide whether to raise, cut, or hold the repo rate.

📉 The Historic Rate Cut Cycle of 2025 — What Happened

Here is the complete repo rate journey:

- January 2025: Repo rate at 6.50%

- February 2025: RBI cuts by 25 bps → 6.25%

- April 2025: RBI cuts by 25 bps → 6.00%

- June 2025: RBI cuts by 50 bps → 5.50%

- December 2025: RBI cuts by 25 bps → 5.25%

- February 2026: RBI holds at 5.25%

- April 2026: RBI holds at 5.25%

- June 2026: RBI holds at 5.25% — neutral stance

What does “neutral stance” mean for you? It means the RBI is saying: “We have already done our part by cutting rates 125 basis points. Now we are watching how inflation and global events unfold before deciding the next move. Do not expect a rate cut or hike anytime very soon.” For borrowers, this means your EMI is stable and not expected to rise or fall in the immediate near term.

💰 How the Repo Rate Directly Controls Your EMI

The connection between the repo rate and your EMI is direct — but only if your loan is structured correctly. Here is what you need to understand:

EBLR — External Benchmark Lending Rate (The Modern System)

Your EBLR-linked loan interest rate = Repo Rate + Bank’s Fixed Spread

The bank’s spread includes credit risk premium, operating costs, and profit margin. This spread is fixed for the duration of your loan. Only the repo rate portion changes when the RBI revises its policy. So when the RBI cut rates by 125 basis points in 2025, your EBLR-linked loan rate should have fallen by the same 125 basis points — automatically.

MCLR — Marginal Cost of Funds Based Lending Rate (The Old System)

If you took a home loan before 2019, it may still be on MCLR. MCLR is not directly linked to the repo rate — it resets only at your loan’s anniversary date, every 6 to 12 months. This means if the RBI cuts rates today, MCLR borrowers may not see the benefit for another 6-12 months — and even then, only partially.

If you are on MCLR — switch to EBLR immediately. This is the single most important action any home loan borrower can take right now. Contact your bank, ask them to switch your loan to the external benchmark rate. There may be a small conversion fee — but the savings over the loan tenure will be far larger.

📊 Real Numbers — How Much Have Indian Borrowers Saved?

Here is exactly how much the 125 basis point cut cycle of 2025 has saved Indian borrowers — in real rupees:

- ₹30 lakh loan, 20 years: EMI fell from approximately ₹26,000 to approximately ₹23,500 — saving ₹2,500/month or ₹30,000/year

- ₹50 lakh loan, 20 years: EMI fell from approximately ₹43,000 to approximately ₹39,500 — saving ₹3,500/month or ₹42,000/year

- ₹75 lakh loan, 20 years: EMI fell from approximately ₹65,000 to approximately ₹59,000 — saving ₹6,000/month or ₹72,000/year

- ₹1 crore loan, 20 years: EMI fell from approximately ₹78,000-80,000 to approximately ₹68,000-70,000 — saving approximately ₹10,000/month.

These are not small numbers. A family saving ₹6,000 per month on their home loan EMI has an additional ₹72,000 per year for investments, children’s education, or emergency savings. The repo rate is not an abstract economic concept — it is a number that directly determines how much of your monthly income goes to your bank.

🔍 Why Your EMI May Not Have Changed — And What to Do

If your home loan EMI has not changed since 2024, there is a real possibility you are not getting the full benefit of the rate cuts. Here is why this happens and what to do about it:

Reason 1 — You are on MCLR: Switch to EBLR immediately. Call your bank’s customer service, ask about switching to the external benchmark rate. Most banks charge a nominal fee of ₹2,000-5,000 for the conversion — which you will recover in savings within weeks.

Reason 2 — Your bank extended your tenure instead of reducing EMI: When rates fall, many banks automatically extend your loan tenure rather than reducing your EMI — keeping your monthly payment the same but making you pay for more years. Check your loan statement. If your remaining tenure has increased, call your bank and ask them to reduce your EMI instead.

Reason 3 — Your reset date has not arrived yet: Even EBLR loans reset rates at specific dates — usually once every three months. If your reset date is two months away, you will see the benefit then. Check your loan sanction letter for the reset date.

Reason 4 — Fixed rate loan: If you took a fixed-rate home loan, repo rate changes do not affect your EMI at all. Fixed rates offer certainty but you miss out on rate cut benefits. Given the current rate environment, a floating rate linked to EBLR is preferable for most borrowers.

🧮 How to Calculate Your EMI — The Simple Formula

The EMI formula is: EMI = P × R × (1+R)^N / [(1+R)^N – 1]

Where P = Loan Amount, R = Monthly Interest Rate (Annual Rate ÷ 12 ÷ 100), N = Loan Tenure in Months.

In practice, use any free EMI calculator online — BankBazaar, HDFC, or SBI all have free calculators. Enter your outstanding loan amount, current interest rate, and remaining tenure to see your current EMI and compare it with what it should be at today’s rates.

🎯 5 Actions Every Home Loan Borrower Should Take Right Now

- Check if you are on MCLR or EBLR: Look at your loan sanction letter or call your bank. If MCLR — switch to EBLR immediately.

- Check your current interest rate: Compare it with your bank’s current published EBLR-linked home loan rate. If there is a gap — call your bank and ask why.

- Check whether tenure was extended or EMI reduced: Look at your latest loan statement. If tenure has quietly increased — ask your bank to reduce EMI instead.

- Consider prepayment: With lower interest rates, prepaying a portion of your home loan principal has a bigger impact than ever. Even ₹1 lakh prepaid today saves you significantly more in interest over 15-20 years at 5.25% repo rate than it would have at 6.50%.

- Compare banks — consider balance transfer: If your current bank is not passing on the full rate cut benefit, compare home loan rates across banks. A balance transfer to a bank offering lower rates can save lakhs over the loan tenure. Processing fees are typically 0.5-1% of the outstanding amount — calculate whether the savings justify the cost.

For more guidance on managing your personal finances effectively, read our complete guide on Personal Finance for Indians 2026 and our article on Investing for Beginners in India 2026.

🔮 Will the RBI Cut Rates Further in 2026?

The RBI’s current neutral stance means no immediate cuts are planned. The MPC is watching two key factors before making the next move:

- Inflation: If food and fuel inflation remains controlled, the RBI has room to cut further. If inflation rises — particularly due to global crude oil prices or a weak monsoon affecting food prices — the RBI will hold or potentially hike.

- Global uncertainty: The US Federal Reserve’s rate decisions, global trade tensions, and currency movements all influence the RBI’s calculations. A sharp rupee depreciation would limit the RBI’s ability to cut rates further.

Most economists expect the repo rate to remain at 5.25% through mid-2026, with a possible additional 25 basis point cut in the second half of 2026 if inflation remains contained. For home loan borrowers, this means current rates are near their floor for this cycle — locking in a home loan now at current rates may be advantageous before any potential future rate movements.

❓ FAQs

What is the current repo rate in India in 2026?

The current RBI repo rate is 5.25% as of June 2026, held unchanged at the June 3-5 MPC meeting. The RBI cut rates four times in 2025 — a total reduction of 125 basis points from 6.50% to 5.25%.

How does the repo rate affect my home loan EMI?

If your home loan is linked to EBLR (External Benchmark Lending Rate), repo rate changes directly affect your EMI within 1-3 months. When the RBI cuts the repo rate, your bank reduces your interest rate by the same amount — lowering your monthly EMI. If your loan is on MCLR, the impact is delayed and partial.

What is the difference between MCLR and EBLR?

EBLR (External Benchmark Lending Rate) is directly linked to the RBI repo rate — changes pass through to your EMI within 1-3 months. MCLR (Marginal Cost of Funds Based Lending Rate) is linked to the bank’s internal cost of funds and resets only annually. Since 2019, all new floating rate home loans must be on EBLR. MCLR borrowers should switch to EBLR to benefit fully from rate cuts.

Should I choose fixed or floating rate home loan in 2026?

With the repo rate at 5.25% — near its cyclical low — a floating rate EBLR-linked loan is generally preferable. Fixed rates offer certainty but you miss out on future rate cut benefits. If rates rise in future, you can consider switching. Consult your bank or a financial advisor for personalised guidance.

How much will my EMI reduce if RBI cuts rates again?

A 25 basis point (0.25%) rate cut reduces EMI by approximately ₹150-200 per month per ₹10 lakh of outstanding loan for a 20-year tenure. For a ₹50 lakh loan, a 25 bps cut saves approximately ₹750-1,000 per month.

What is the reverse repo rate?

The reverse repo rate is the rate at which the RBI borrows money from commercial banks — the opposite of the repo rate. It is currently 3.35%. When banks have excess funds, they park them with the RBI at the reverse repo rate. The reverse repo rate sets the floor for short-term interest rates in the economy.

📚 Sources

- SMC Insurance — Current Repo Rate India 2026: Live RBI Policy Updates and EMI Impact

- Upstox — How RBI Rate Changes Impact Your Home Loan Interest Rate April 2026

- Asianet Newsable — RBI Policy June 2026: Your EMI Stays Put

- Stashfin — RBI Repo Rate and Home Loan EMI Guide 2026

- PNB Housing — Understanding Repo Rate and Its Impact on Home Loans

- Business Standard — RBI Rate Cut: EMIs May Fall to ₹68,000-70,000 for ₹1 Crore Home Loan

- Rustomjee — Repo Rate and Reverse Repo Rate 2026