Here is a fact that should make every salaried Indian angry: the Sensex grew from 1,000 in 1990 to 77,000+ in 2026 — a 77 times return in 36 years. If your parents had invested ₹1 lakh in the Indian stock market in 1990, it would be worth ₹77 lakh today. They probably did not. Most Indians did not. Because nobody told them how. Because the stock market was seen as a rich man’s game, a gambler’s den, something for people in Mumbai with Bloomberg terminals and expensive suits. That story was always a lie — and in 2026, with a smartphone, ₹500, and 15 minutes, any Indian can start building real wealth in the same market that made India’s richest families their fortunes. Here is exactly how.

🤔 The Truth About the Stock Market That Your School Never Taught You

Most Indians think the stock market is gambling. It is not. Here is the difference: gambling is a zero-sum game — for every winner, there must be a loser. The stock market is not zero-sum. When you buy one share of Tata Consultancy Services, you own a tiny fraction of a company that employs 600,000 people, generates billions in revenue, and grows its profits year after year. As TCS grows, so does your investment. No casino does that.

The Sensex — Bombay Stock Exchange’s benchmark index of 30 largest companies — and the Nifty 50 — NSE’s index of 50 largest companies — are the two numbers that tell you whether the market is going up or down on any given day. When news channels say “markets fell 500 points today” — they mean one of these indices fell. These numbers are your daily report card on the health of India’s largest companies.

Here is the most important thing nobody tells beginners: you do not need to understand every company, every balance sheet, or every market movement to make money in the stock market. You just need to understand one concept — compound interest — and one instrument — an index fund. Everything else is optional.

💰 The Number That Will Change How You Think About Money Forever

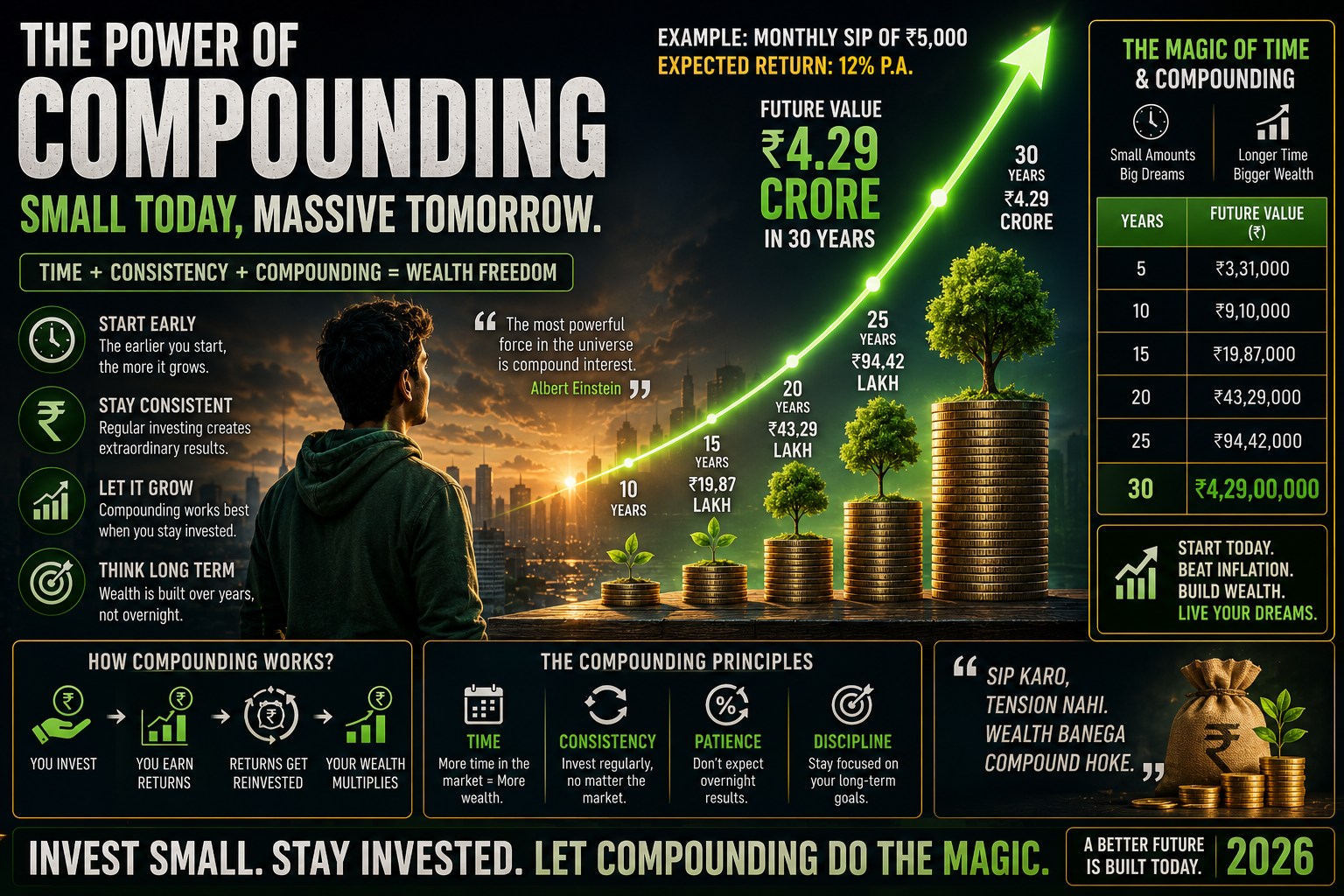

A ₹1,000 SIP started at age 25 in a Nifty 50 index fund, compounding at 12% annually, becomes approximately ₹75 lakh by age 60. The same ₹1,000 monthly SIP started at age 35 — ten years later — becomes only ₹20 lakh by age 60. The difference between starting at 25 and starting at 35 is ₹55 lakh — earned not by investing more money, but simply by starting earlier.

This is the power of compounding — what Einstein allegedly called the eighth wonder of the world. Your returns generate their own returns. ₹1,000 earns ₹120 in Year 1. That ₹120 also earns returns in Year 2. By Year 30, compounding has done far more work than your original investment. Time is the most valuable ingredient in wealth creation — and it is the only one you cannot buy back.

The reason most Indians miss this opportunity is not lack of money. It is lack of starting. Every year of delay costs you more than you realise. The best time to start was when you got your first salary. The second best time is today.

📱 How to Actually Start — The 5 Steps Every Beginner Needs

Step 1 — Open a Demat and Trading Account (15 Minutes, Free)

A demat account is mandatory for investing in stocks. It acts like a digital locker where all your shares and investments are stored safely in electronic form. Without a demat account, you cannot hold stocks in India. A trading account is the bridge between your bank account and demat account — it is used to place buy and sell orders.

Best platforms for beginners in 2026:

- Groww — Most beginner-friendly interface. Free demat account. Zero brokerage on mutual funds. Best for first-time investors.

- Zerodha — India’s largest broker. ₹20 flat brokerage per trade. Excellent educational resources. Best for those ready to invest regularly.

- Upstox — Low cost. Good mobile app. Backed by Ratan Tata. Good alternative to Zerodha.

Documents needed: Aadhaar card, PAN card, bank account details, and a selfie. The entire process is digital — no branch visit needed. Most accounts are active within 24-48 hours.

Step 2 — Start With an Index Fund — Not Individual Stocks

Why index funds first? Because they are diversified — if one company falls, 49 others cushion the impact. They have the lowest costs — expense ratios under 0.2%. They require zero stock-picking expertise. And historically, most professional fund managers fail to beat a Nifty 50 index fund over 10 years. If the experts can not consistently beat it, the beginner certainly should not try to.

Step 3 — Set Up a Monthly SIP (Systematic Investment Plan)

A SIP automatically invests a fixed amount every month — on a date you choose — into your chosen fund. Set it up once. Forget it. Let it run for years. This is the single most powerful investing habit available to any Indian — and it requires zero effort after the initial setup.

Start with whatever you can afford — ₹500, ₹1,000, ₹2,000. The amount matters less than the consistency. Before buying individual stocks, start with a Systematic Investment Plan in an index fund or diversified equity mutual fund. This is the fastest way to get market exposure without needing to research individual stocks. Increase the SIP amount by 10-15% every year as your salary grows.

Step 4 — Understand Taxation Before You Invest

Gains from stocks and equity mutual funds are subject to capital gains tax — 20% for short-term gains (held less than a year) and 12.5% for long-term gains above ₹1.25 lakh per year. This means if you hold your investments for more than one year, your first ₹1.25 lakh of gains is completely tax-free every financial year. Long-term investing is not just good strategy — it is also more tax-efficient.

Step 5 — Never Touch Your Investment During a Crash

Market crashes are inevitable. The Sensex has crashed multiple times in the last 30 years — during the 2008 global financial crisis, during COVID-19 in 2020, during multiple corrections since. Every single time, the market recovered and went higher than before. Every investor who stayed invested made money. Every investor who panicked and sold during the crash locked in their losses.

The correct response to a market crash when you have a SIP is: nothing. Continue your SIP. Your monthly investment now buys more units at lower prices. When the market recovers — and it always has — those cheap units become worth significantly more. The crash is not a threat to your SIP. It is a discount sale.

📈 The 3 Types of Investments — Which One Is Right for You

1. Index Funds and ETFs — Best for Beginners: Tracks a market index like Nifty 50. Automatically diversified. Lowest cost. Zero expertise needed. Best for 90% of beginners. Start here.

2. Actively Managed Mutual Funds — Better for Intermediate Investors: A professional fund manager picks stocks on your behalf. Higher costs than index funds (expense ratio 1-2% vs 0.1% for index funds). Some managers consistently beat the index — but most do not over long periods. Good for investors who want professional management and are comfortable paying for it.

3. Direct Stock Investing — For Those Ready to Research: You pick individual companies based on research. Highest potential returns — and highest risk. SEBI tightened F&O eligibility criteria in 2025 — beginners are advised to trade only in equity delivery (not derivatives) for the first 12 months until fundamentals are mastered. Do not start here. Build confidence with index funds first, then graduate to individual stocks after 12-24 months of investing experience.

🚫 The 7 Mistakes That Destroy Beginner Investors in India

- Mistake 1 — Investing money you need within 12 months. Stock markets can fall 30-40% in a crash. Only invest money you will not need for at least 3-5 years. Emergency fund first — always.

- Mistake 2 — Buying penny stocks. Penny stocks — shares trading for ₹5 or ₹10 — feel exciting because you can buy hundreds of them. Do not do this. Cheap stocks are usually cheap for a reason — the company is terrible.

- Mistake 3 — Following tips from WhatsApp groups. “Buy this stock tomorrow — guaranteed 50% return” is either fraud or ignorance. SEBI regulations prohibit unregistered investment advice. If someone is giving you guaranteed return tips on WhatsApp, they are either going to jail or they are going to take your money first.

- Mistake 4 — Selling during a crash. This is how retail investors consistently lose money. They buy when the market is high (after reading positive news) and sell when it crashes (after reading negative news). Exactly backwards.

- Mistake 5 — Checking your portfolio daily. Daily checking leads to emotional decisions. Markets fluctuate every single day. Your 20-year investment should not be managed based on what happened today. Check quarterly — not daily.

- Mistake 6 — Not diversifying. Putting all your money into one stock — even a great company — is unnecessary risk. Index funds solve this automatically by spreading across 50 companies.

- Mistake 7 — Starting too late. Every year of delay costs you compounding returns that cannot be recovered. The regret of not starting is always more painful than the discomfort of starting without knowing everything.

🎯 Your Action Plan — Start This Weekend

- This weekend: Download Groww or Zerodha. Complete KYC with Aadhaar and PAN. Takes 15 minutes.

- Day 2: Transfer ₹1,000 to your trading account.

- Day 3: Search “Nifty 50 Index Fund” — choose a Direct Plan with expense ratio below 0.2%. Start a SIP of ₹500-1,000/month.

- Every month: SIP runs automatically. Do nothing.

- Every year: Increase SIP by 10-15%. Review portfolio once every 6 months.

The Indian stock market has created more wealth for patient investors than any other asset class over the last 30 years. The door is open. The tools are free. The minimum investment is ₹500. The only barrier left is the decision to start. For more on building wealth, read our guide on Personal Finance for Indians 2026 and our complete guide on Investing for Beginners in India 2026.

❓ FAQs

How much money do I need to start investing in the stock market in India?

You can start with as little as ₹500 through a mutual fund SIP. For direct stock investing, you need enough to buy at least 1 share of your chosen stock — some quality stocks trade under ₹100-200. There is no minimum balance requirement for a demat account on most platforms.

Is the stock market safe for beginners in India?

The stock market carries risk — values can fall in the short term. However, over 10+ year periods, the Indian stock market has consistently delivered positive returns. The risk reduces dramatically with time horizon and diversification. Starting with a Nifty 50 index fund SIP is the safest way for beginners to get stock market exposure.

Which app is best for stock market beginners in India?

Groww is the most beginner-friendly — simple interface, free demat account, zero brokerage on mutual funds. Zerodha is best for those ready to invest regularly in stocks — ₹20 flat brokerage, excellent educational resources. Both are SEBI-registered and trusted by crores of Indian investors.

What is the tax on stock market profits in India?

Short-term capital gains (stocks held less than 1 year) are taxed at 20%. Long-term capital gains (stocks held more than 1 year) above ₹1.25 lakh per year are taxed at 12.5%. Gains below ₹1.25 lakh per year from long-term equity investments are completely tax-free — making long-term investing significantly more tax-efficient.

📚 Sources

- Univest — How to Invest in Stock Market for Beginners India 2026

- Univest — Stock Market for Beginners India 2026: Complete Guide

- PaisaTech — How to Start Investing in Stock Market India 2026

- GTU Ranker — How to Start Investing in Stock Market for Beginners 2026

- MintByte — How to Invest in Stock Market India 2026

- CommerceCare — Stock Market Basics for Beginners 2026